Crossroads

An Accidental Stop in the Silicon Heartland

The uproar over datacenters is cascading across the nation. Despite 70% of Americans being opposed to datacenters, per Gallup, our tech elite and their funders are putting all their eggs in its basket. We have often talked here about how the AI narrative arrived just in time in 2023 to work in conjunction with the Fed’s funding facility (BTFP) to “save” the stock market and restart the economy after SVB’s failure. This happened just as many of us working in tech realized that AI was not yet affordable enough to truly replace workers. Offshore developers and back-office workers became the play.

How bizarre is it that what purportedly “saved” the economy is also forecasted to largely replace the worker? When almost 70% of GDP in the United States relies on consumption, how exactly is that going to work? While I disagree with the tech talking heads on timeline and scale for AI to create the efficiencies imagined, they’ve convinced quite a few that this is the case. Yes, yes, our technocracy dreams of universal basic income (UBI) and days spent painting or doing origami, but how realistic is that really? And, have you met humans? What happens to them when they don’t work?

The labor force participation rate peaked in 2000. Since then, it has fallen significantly. At the same time deaths of despair have increased to the highest level since 1900.

Deaths of despair are defined as “deaths by suicide, drug and alcohol poisoning, and alcoholic liver disease and cirrhosis.” What pray tell could cause such despair? When I visited San Diego’s homeless encampment, O-Lot, and talked to Anthony, he told me how grateful he was that he had a tent. However, he really wished the O-Lot operators could help him find a job. That wasn’t on the agenda. You get paid by unit in the public/private social welfare schemes here in the U S of A which means Anthony staying in that tent matters more than finding him a job so that he could actually forge a pathway out of homelessness. The perverse incentives that permeate our day-to-day existence mean that we are spinning our wheels in what feels like hell. The rich get richer, the poor get poorer and reality resembles a horror movie.

While the technocracy celebrates the move to this dystopian future, our students have something else to say. At a recent commencement speech, Eric Schmidt, the former CEO from Google, got mercilessly booed when he mentioned AI. It cheers me to know that our younger generations will not sit quietly while the top 1% continues to rape and pillage the system. The more research I do into this datacenter boom the more I realize how crazy it really all is. Some newcomers may be wondering why I’m talking about AI in these pages. The datacenter story is truly a real estate story despite how it’s being peddled. A good deal of our speculation in the housing market as well is due to carpetbaggers drooling over boomtown profit possibilities. Every city surrounding these projects has seen increased speculation and building. The Midwest in particular became seriously infested between 2023-2025 as investors saw it as the last frontier for fix and flipping due to lower home prices.

Today’s post will feature a look-see into New Albany where it all started for Ohio in particular. When on my last trip enroute to Nashville I happened to stop there by accident, forgetting that New Albany was the location of the Intel project I had been tracking since 2022. When I’m on these trips, I don’t plan ahead as I never know exactly where the road will lead. I’m often punching locations into my Bonvoy app while driving 70+ mph to find the nearest spot when I’m ready to stop. I prefer Courtyards because they (should) have a food option, and I’m often too tired to leave the hotel. I arrived in New Albany at dusk, following one of those dazzling orange-red Ohio sunsets, and was surprised at how many folks were hanging in the Bistro. In the spots where I stopped previously on this trip, I had been the lone customer in what felt like empty hotels. I asked the hotel manager why it was booming, and she replied, “datacenters.” She proceeded to tell me that it had been like that for three years. She pointed to a gentleman in a large cowboy hat who I had previously heard telling a fellow traveler that he was from Texas, “he’s been here every week for three years.” Seemingly, I had stopped in one of the few places in the country which was still booming. Many of us have seen the charts and figures that show the only thing holding up the economy is AI which was perfectly illustrated by the scene I encountered.

Before we get to the meat and potatoes of today’s post, let’s review April existing home sales which were nothing to write home about. Side note: for those paid subscribers who filled out the form to receive breaking news alerts for existing and new-home sales, expect your first email when new home sales are published on May 28th. Existing home sales of 354,000 in April non-seasonally adjusted were up 1.43% Year-Over-Year (YoY) and 7.60% Month-over-Month (MoM); #4 for the worst April since 1999 behind 2009, 2023 and 2025. Seasonally adjusted, sales were up 0.00% YoY and 0.2% MoM. We were deep in the tariff tantrum last year and stocks were taking a beating unlike this month where we saw an all-time high in the S&P, so minor improvements are to be expected. Nonetheless, existing home sales YTD are only running 0.78% ahead of 2025 (worst sales since 1995), but -1.68% behind 2024. The 27-year average for April existing homes sales is 444,500; sales are -20.36% below the average. The average increase in existing home sales from March to April is 8.83%, so this MoM increase is below average. Looking through the prism of our last housing crisis, existing home sales of 458,000 in 2007 increased 5.05% from March to April. April 2026 sales are -22.71% lower than April 2007. In 2008, existing home sales of 364,000 increased 15.19% from March to April. April 2026 sales are -2.75% lower than April 2008; YTD sales are running -0.59% behind 2008. The median sales price for existing homes in April was $417, 700; March was revised up slightly to $409,100 from $408,000.

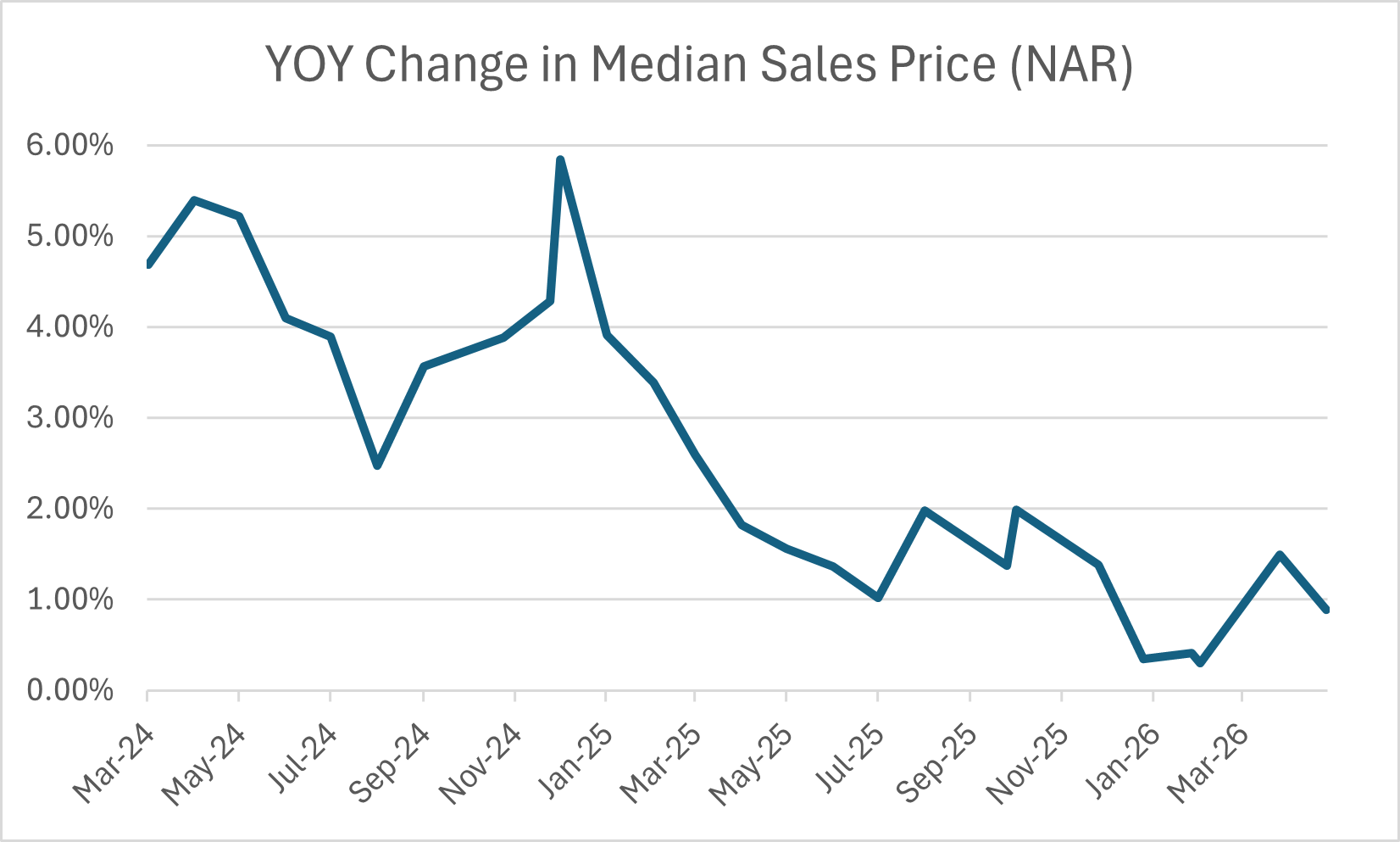

The median sales price was up 0.89% YOY (compared to last month at 1.41% YoY) and up 2.10% MoM; on average since 1999, existing median sales price increase by 2.36% between March and April. According to NAR, existing home supply ended March at 4.4 months of supply, versus 4.2 months in March (revised up from 4.1).

Below, I will discuss the regional differences in sales as well as the signals from the distribution of sales by price. These details provide clues as to what’s next for the areas of the country that have not seen widespread YoY price declines. As mentioned, I will share my research into New Albany, OH, its numerous datacenters as well as what this could mean for housing and the economy. Want to guess which famous mogul is behind the industrial park there? It’s spicy. And, finally, I’m excited to share that I will now be posting the commercial real estate articles I’ve been publishing at Unicus Research here. The crew at Unicus has generously given me permission to do so. For those interested in their detailed analysis on markets, I recommend their Confidential Insights reports. My readers will receive a 20% discount. I encourage you to check it out and if you wish to subscribe, please fill out this short form. In addition to my New Albany analysis, you will also find below my recent article on private credit and its tentacles, which are tightly wrapped around this datacenter boom.

Without further ado…