Ice Skating on a Frozen Lake

Last year I ended my 2024 look-forward with the below words of advice as we faced what we all knew was going to be a very turbulent year:

In summary, it feels as if 2024 will be 2023 continued at an elevated pitch, especially on the political front. Are we in a recession? Is a recession coming? Will tensions in the Middle East, with China or Russia escalate? Will more robots attack workers? I have no definitive answers for these questions, but from what I’ve observed from weeks spent on the road, thousands of hours reading and researching and tracking data, the path for housing is a correction that will play out over multiple years with 2025 likely seeing the largest price declines. If, however, some serendipitous good fortune comes our way to pave a productive path to home ownership for our younger generations, I for one will be ecstatic. And, I will be the first one to let you know. Until then, discerning eyes and ears are the order for the day and year ahead.

In many ways I don’t feel like 2024 really happened. If 2023 was a blur, 2024 just felt like a high-speed car chase that went by even faster than 2023. So many headlines, so much drama, so many limited hangouts, so many frauds. Fact and fiction became impossible to discern, and by the end of 2024 I think we are all just a bit exhausted.

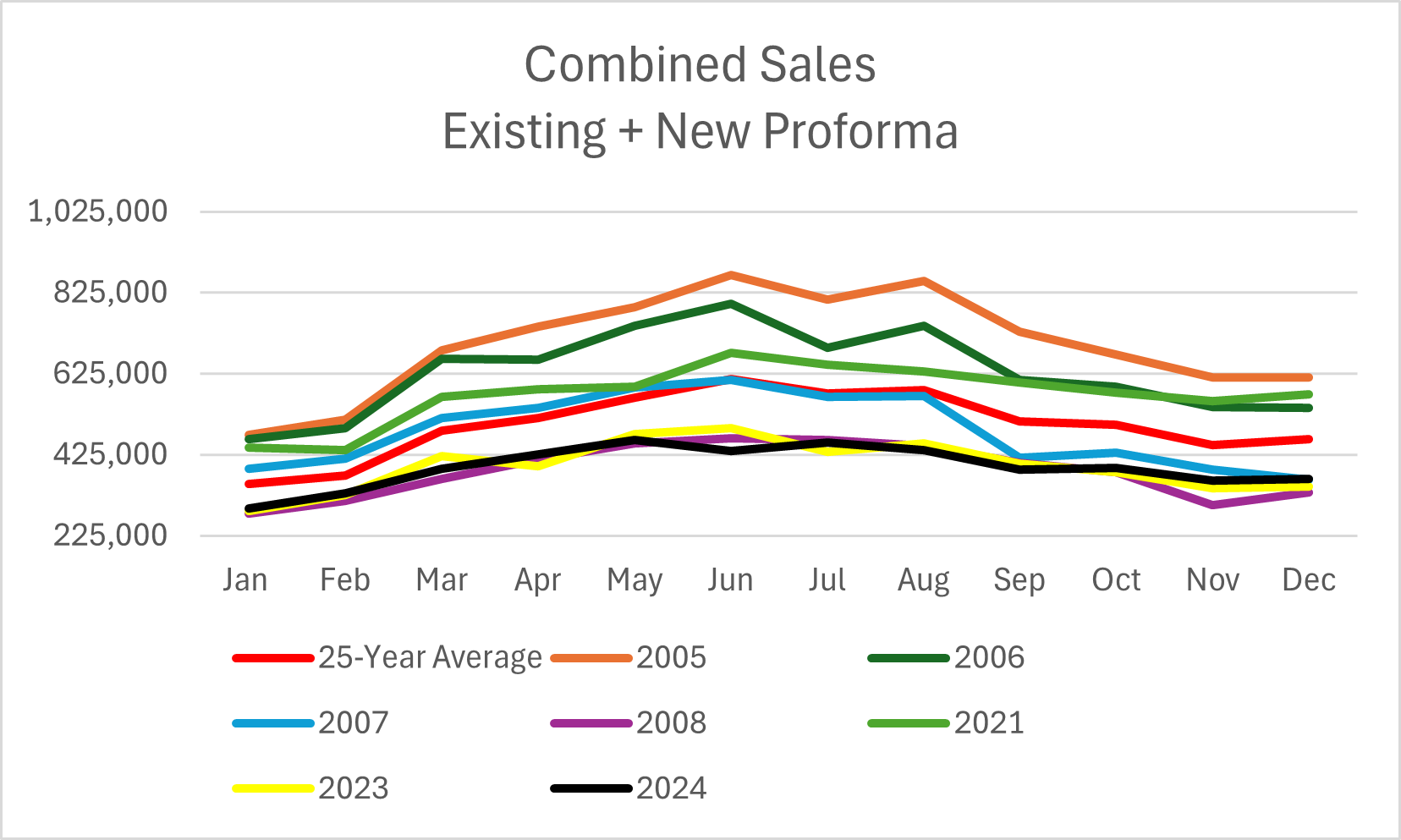

When looking at home sales and data we roughly just skated on the back of the frozen market to do a repeat of 2023 despite several instances of “much ado about nothing” regarding rate cuts.

It feels as if we have just been ice skating on the same frozen lake for two years:

Don’t get me wrong, in his fake word pivot in December of 2023, J Pow certainly brought out the sellers, but not so much the buyers. Similarly, as rates moved down over the summer, the listings made a steady march to the MLS.

That increasing inventory and lower rates over the summer led to a bump in sales at the end of the year which was driven primarily by the West who realized - like Florida, Texas and NAR - it was time for price cuts.

Pending home sales came out this week forecasting a higher December, but remember this series tracks signed contracts, not closings. Likely we will have a higher December than 2023 for existing home sales. Last December we fell below 300,000 sales, reeling from the rate peak of our COVID-boom cycle (thus far) in October 2023.

Combined sales for 2023 were 4,753,000. If we use the Pending Home Sales Index and historical sales for new homes to extrapolate, the optimistic view is that we likely end 2024 with 4,726,800 in combined sales. That will be less than 2023 and every other year since 1999 except for 2008-2011 which were the absolute lowest levels during the GFC.

More and more I’ve started to realize that the narrative machines have been working overtime to keep us from perspective of what we have been through in the last 20 years, and honestly much longer than that. I cannot count how many times I was told starting in late 2021 that I was a lunatic for even discussing the previous housing crash or similarities to 2008. The biggest gift I got in 2025 was the existing home non-seasonally adjusted data that goes back to 1999. The data was once available for free, but they charge now. Being able to look at what was happening in context mattered. With that context you can see that the COVID boom never reached the heights of the last boom.

Once I could set aside all of my industry indoctrination, the credit quality gospel singing and my ever-present need to not look like a fool, I could see that nothing changed since the GFC - the mania just got worse. The roles of some of the players have changed and Wall Street as landlord was introduced at scale - they had already gotten started in 2002 through the single-family non-performing loan sales program - but the speculation and push of housing as ATM has not changed. I know, I know they keep telling you there is lots of equity and there haven’t been equity withdrawals, but don’t let artificially inflated home values fool you. There has been significant equity withdrawal including the 1.8M payment deferrals that aren’t being tracked anywhere I can find. Additionally, the cashout refinances that everyone piled into during the COVID refi boom look ok right now, but just wait until we actually have comparables as some of these listings with drastic cost reductions sell.

The lipstick color has changed, but the underlying mechanics and motivations have not. For those like me who went through absolute hell last time thinking they were piecing the financial system back together into something better, well yet again, we were duped. It’s never fun admitting you’ve been a useful idiot, but it’s better than being in denial. What is very obvious is that lower rates had diminishing returns this time around. So why are there so many people addicted to the rate narrative? That is the question in my opinion.

Although population has increased by roughly 12% since 2007, we had lower sales in 2023 than 2007. I mention this often, but this is how you know they are trying to pull the wool over our eyes as to their ability to save the situation or drive any outcomes with rate decisions. By the by, if anyone is looking for something to give me in 2025, I would love the historical listing data as well.

Last year I postulated that the election would determine the course of the year as there was and is so much need on both sides of the aisle to keep the housing and securitization markets churning. In my opinion one of the reasons we ice-skated through 2024 is that reality had to be suspended through the election blitz. When we look back at this time period though, I believe the hurricanes will surface as having an outsized impact on what happens next. Will the hurricanes - Beryl, Debby, Helene and Milton - which slammed into 8 states get their due in approved history books? Perhaps not, but just as I could dig and uncover the importance of the 1927 flood, someone like me in the future will be able to unearth and ascertain the materiality of these events.

There simply is no question that housing is unaffordable and out-of-reach for most. This year, the percentage of first-time homebuyers fell to 24% according to the National Association of Realtors (NAR) - the lowest since they began tracking in 1981. We simply do not have enough rich people to sustain this housing market. In my weekly tracking, I see luxury sitting and sitting. Asset holders are also coming under pressure as the costs to insure and maintain have skyrocketed, not to mention property taxes. What are the drivers and levers that we must watch to determine where we are so we can make the necessary decisions to protect our interests and values while paving the way for our collective children? To understand what’s ahead in 2025, we will review deep-dive metrics for November including inventory, sales, prices, days-on-market and credit metrics for the regions and cities I track as well as top-five rankings in each category. Speaking of inventory. Please go back and read this stack I wrote after returning from two months of touring in Florida in the summer of 2023. My Substack was published on October 3, 2023. Newsweek just published this on December 31, 2024:

In addition to the above metrics, I will provide an update on delinquency in hurricane-impacted areas. It ain’t good.

To access your 2025 roadmap, please turn here…

Keep reading with a 7-day free trial

Subscribe to M3_Melody Substack to keep reading this post and get 7 days of free access to the full post archives.