On the Road Again

3,195 miles driven, thirteen states and eight hotels…that’s my last two weeks summed. Having several commitments in the East and few options to make it logically work from my regional airport, I decided it was time to see what I could see from the road (again). Those I’ve related this to look at me as if I’ve grown an extra head. Worth it, it was, due to the critical intel I gathered while on this last trip.

I took my very first cross-country road trip from Mississippi to California for Christmas when I was five years old. I would be 19-years old the first time I was behind the wheel - adding in points northwest such as Wyoming, Glacier and Seattle. You might say it’s in my blood. My grandmother was known to drive from California to Mississippi by herself with only coffee and cigarettes to fuel her. I don’t partake in either, but I do make sure I travel with plenty of Earl Grey.

You can see a lot on the road. Things you cannot see if you fly in, grab an Uber and go straight to your destination. If you are super-observant and decide to look up from your phone as your Uber transports you to your destination instead of catching up on email and texts you missed because the internet was spotty on the flight, you will notice all the cranes and traffic. However, much of what has happened in this country post-Covid is hard to spot based on those quick trips. Let’s say you are flying to Phoenix to check out a development site there. Due to the walls along the highways constructed to reduce noise, you have no idea what’s going on behind those walls. Unlike, say, driving from Austin to San Antonio where you can see almost everything from the highway. You cannot of course though see the sheer madness of Round Rock, TX where there is a new-build subdivision on every block unless you exit the highway. If you are “prospecting” either to invest in real estate or even write about the market, your guide will take you to their choice spot, likely even oblivious themselves to what’s happening in the rest of the city. In the three years I’ve been posting on social media following my very first road trip, I’ve had to search every data nook and cranny to understand why others could not see what I was seeing. After all that searching, I can say more confidently, they are just not looking. I will leave it to others to ponder why that is.

So, although the road is long and the food is really bad, I do these trips to see firsthand what is happening out there. And, in so doing, I am privileged to also see what is best about our country. The sheer beauty and regional variability in the United States is hard to fathom unless you have traversed it yourself. You also get to talk to real people versus those that pontificate ceaselessly on social media. If more people just did that these days, our shared struggle would be so obvious empathy would be involuntary. On the road, you encounter those that are plugged into the corporate cortisol machine forced to believe that a life constantly moving and shaking is “a life”. Never mind that although their high-stress job ensures they can pay their mortgage on that fancy house, they never stop to enjoy it for more than a couple of days a week. You also see those that are working twice as hard as their colleagues in low-paid service jobs, desperate to retain their job and feed their kids or pay for school. On the other end of that spectrum, you come into contact with those from the younger generations working in service jobs who struggle to properly function. They have trouble completing the simplest tasks. Any variation to the three things they’ve mastered causes a complete crashout. They can’t look at you or engage in small talk. What you see above all is that if we don’t change our ways soon, something beautiful will be lost. And, by the by, you get to see wonderfully weird and unexpected things such as a dozen General Lees and Rosco’s cop car traveling west on I-40 for the Cooter’s Hazzard Run from Pigeon Ford to Nashville.

What a welcome flashback to fond, childhood memories of the Dukes of Hazzard, especially Uncle Jesse. As the war drags on, I’m reminded more and more of the 70s. No matter the latest barbs being traded on cable news, this situation with Iran is serious. I recommend this episode with Christine Guerrero on Coffee and a Mike if you want to understand the impacts we will feel even if the war ends today. Christine is a straight shooter and a petroleum engineer. Engineers have a very specific way of thinking that I believe is helpful in times like this. If you want to travel back in time and watch a clip which could inform our potential future, check out this Johnny Carson monologue from 1973.

Just because I decided to do my own mini, modified canonball run, breaking news in housing and credit did not downshift into neutral. After looking at March Redfin and NAR results, I thought we might be setting up for a completely frozen spring again. The price weakness was showing but the lower sales in many areas was continuing to cause price contortions. The trend was completely obvious in March results as cities with the highest median home sales price increase were the ones with lower sales. Then, we got some very interesting data from multiple sources that makes me think things are indeed speeding up despite the seasonal price firming we saw in results reported from NAR and Redfin.

Before we begin, let’s quickly review some of the important, recent developments in banking and credit. When the world runs on debt, the credit corner is one where the floodlight should be fixed. While I was on the road, we had our next installment in the series entitled Bank Failure Friday. Community Bank and Trust, a small Georgia lender, was closed on May 1st by the Georgia Department of Banking and Finance. For a deep dive into what happened there, I highly recommend Nobody Special’s recent video. There are two very important takeaways from this bank failure which will cost the FDIC insurance fund $97M. Firstly, unlike with SVB, the FDIC is not defacto covering deposits over $250K. Additionally, likely what caused Community Bank and Trust, who participated in government-guaranteed USDA and SBA lending, to get in over its skis, was a misguided faith in financial “innovation” and automated underwriting. I have been warning about this since 2022. We cannot completely Henry Ford credit. Those automated systems can be easily gamed. The lack of real oversight also means that no one is catching the issue until the loans stop performing. One reason that we have yet to see the real warts and fraud in FHA (gubn’t subprime) is because of that overly aggressive partial claim program where you were able to go back to the till over and over again…and our investors did just that. Those fraud bombs are incoming. As stress begins to mount in the agency prime books this will become more and more obvious, and all that credit quality gospel singing will be revealed for the performance it truly was.

Speaking of performance - at an event in NYC, I got to hear the private credit party line from a famous Wall Street personality. When you know the “what” is not accurate based on your own research, it’s actually fascinating to watch “how” they deliver the message. There is a specific cadence to it that I’ve now programmed into my BS detection meter. The problem with the current demand that you believe private credit is not a systemic issue is that most of the analysis is focused on the software sector only. Firstly, many of these analysts discussing the topic would not be able to code their way out of a paper bag so they don’t understand any of these investments. And secondly, private credit played everywhere, especially in real estate. Commercial real estate in particular caught their eye. So, when you get news like the below, you have to pay attention.

Our financial system is a highly connected organism. Just like the root system that supports the trees in your front yard, an entire universe is hidden from view. Private credit may not end up causing a systemic failure, but anyone who acts certain that it won’t should be considered highly suspect. Certainty in times like this is foolhardy.

The entire system hinges on us being able to buy stuff. As prices and input costs stay elevated, many consumers will no longer be able to buy stuff. Those companies that are not able to largely pivot to luxury consumers or absorb higher costs know this too well.

McDonald’s miss in sales expectations today also illustrate just how stretched the consumer at the lower end of the K is.

Source: University of Michigan

At the moment, the bottom third who does not benefit from all-time highs in the stock market are much worse off than a year ago. Remember, though, this is the picture as of now when most are in no way pricing in the true risk from the war in Iran. Fertilizer shortages and forthcoming increases in input costs mean higher food prices in the future. Additionally, as more and more consumers tap out due to layoffs, increased property tax and insurance and failed investments, the conditions will deteriorate even further. It’s not just large companies closing. It’s small(ish), family-owned businesses as well.

Want to guess where one of the stores Lammes has closed is located? Hint - I mentioned it earlier. Okay, okay. I won’t make you work: Round Rock, TX.

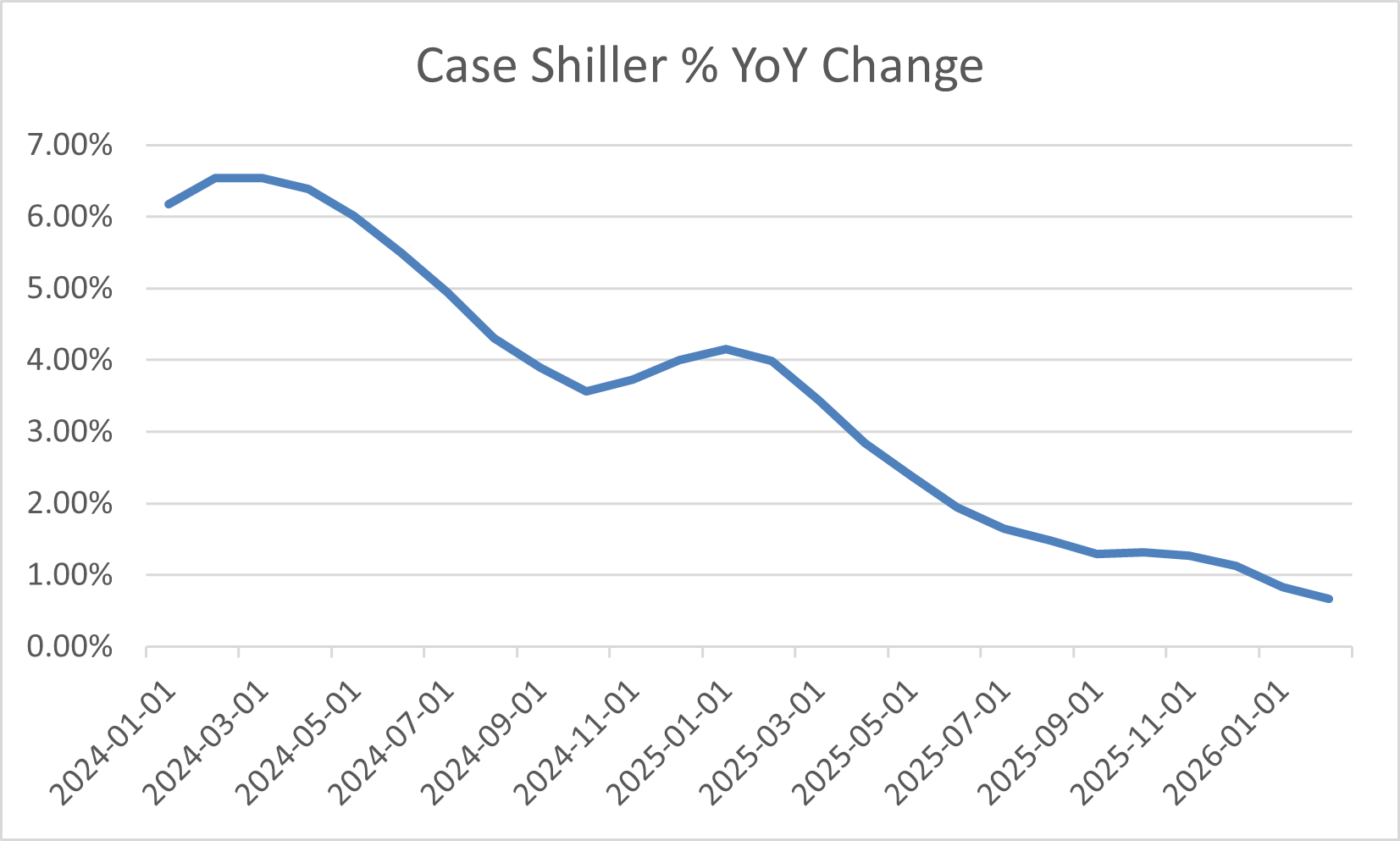

It’s all connected. Looking at one or two data points in isolation will never show the true picture. Nonetheless, THE data point many in the housing industry hang their hats on just printed its lowest YoY increase since 2023.

Source: FRED

As a reminder, the Case Shiller index is significantly delayed, uses repeat-sales, excludes condos and new homes and is a 3-month rolling average. No matter which way you shake it, the trend here is clear. For those banking on rate cuts to save the housing market, rising prices will have something to say about that. What we really need is lower home prices and good jobs. Bankruptcies large and small will not help with the employment picture. We might see a moderation in this decline during the season as we did last year but based on other data received which I will discuss below, this series is likely set to go negative by Q4 2026, or sooner.

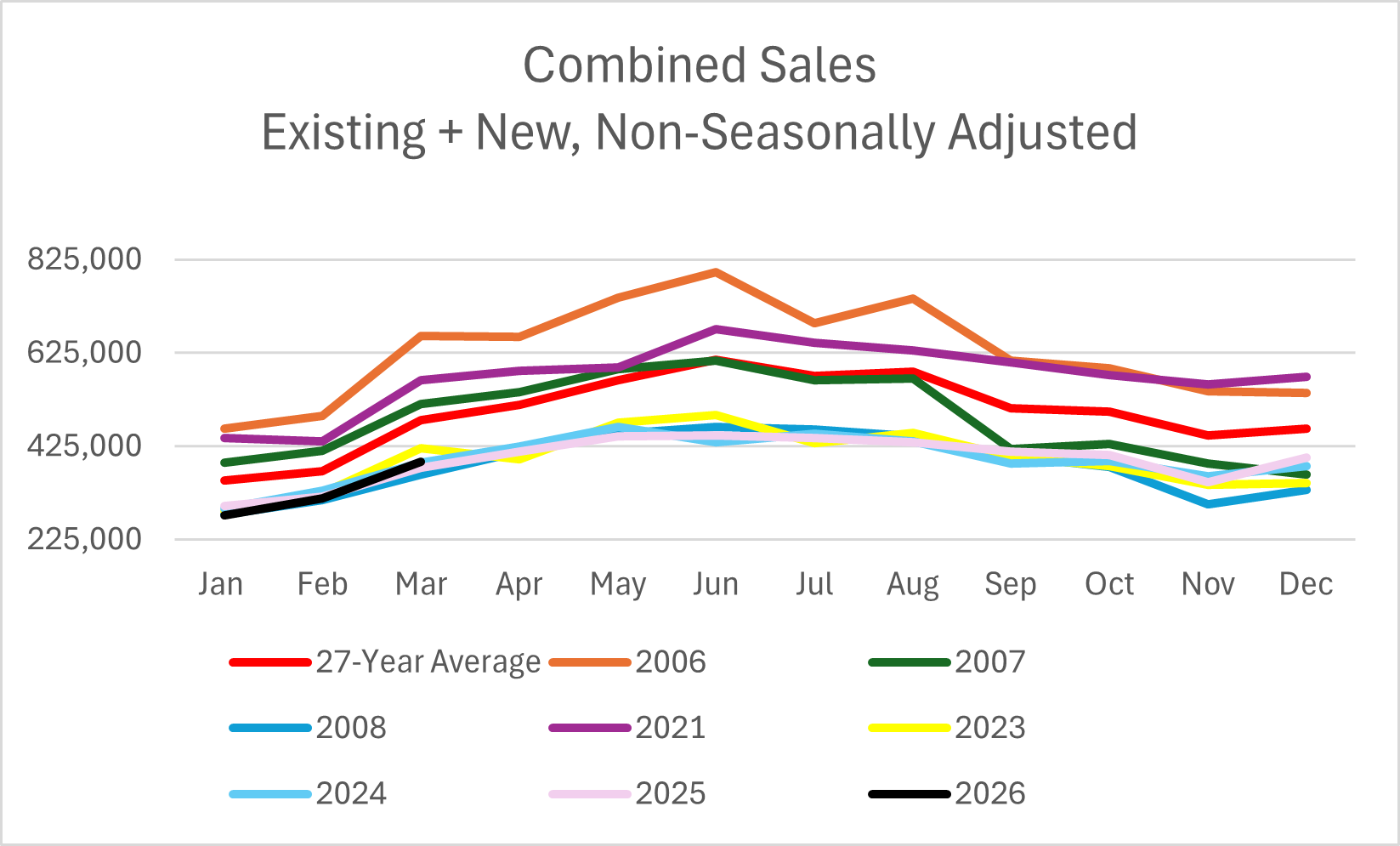

In a recent interview with Adam Taggart's Thoughtful Money®, I could not contain my nerd excitement about changes or anomalies I’m seeing in two different data sets. My excitement of course is not about the trouble ahead, but more about a breakout in pattern. Believe it or not, I taped that interview prior to us receiving new home sales (finally) for February and March. Boy howdy did those jolt me out of my seat. For some time, I’ve been making the argument that higher sales will bring lower prices. We’ve often seen evidence of this, but these results were loud and clear. Below, we will delve into those new home sales results as well into the Freddie Mac home price index which also surprised. Additionally, legacy media weirdly and finally picked up the default thread. Why now and what’s to come? What many fail to comprehend is that our economy is fueled on growth. Just meeting last year’s metrics does not suffice. In housing, home prices have to climb to keep the shell game going.

Low volume will not adequately feed the machine such that higher prices are sustainably achieved. When housing is no longer affordable for most of the market, including investors, there is no path to continual price gains. When demand looks like the below, hope is not a strategy:

Yes, those invested in rentals might find the above encouraging. However, your declining rents, increased costs, rising vacancy and inability to cashflow should temper that excitement. Finally, I will share the M3 Price Tracker as well as lists of cities where we are seeing motivated, distressed and depressed selling with cities in the Northeast making the lists. Inventory in both the Midwest and Northeast continues to grow at an accelerated pace. In cities like Stamford, CT and Portsmouth, NH low inventory isn’t even stopping the price declines.

Let’s not tarry…