ADD For Both You and Me

I feel as if time has rolled over me and I’m now flat as a pancake with little idea how to reanimate, catch back up, as headlines scream at us, tearing our attention from one thing to another at warp speed, creating ADD exponential as we try to keep up and anchor in some palatable reality: Israel/Hamas conflict; China and a new Chinese pneumonia; a bizarre melodrama regarding our potential new Robot overlords; UFOs; cyberattacks; the deaths of Kissinger, Munger, O’Connor; sunspots, and I could go on and on. Remember Dodgeball? No, not the movie….many of you may not, but we actually used to play a game in PE (aka gym class) where we threw balls at other people hoping to hit them. And then there’s the wonderful scene in Freaks and Geeks when Sam stands all alone waiting for his entire gym class to let loose on him. Classic.

Anybody else feel this way? Anthony Dilweg put it a little bit differently in one of the best interviews I have heard on the Commercial Real Estate issue to date with Jack Farley. In our financial system and reality today you have to keep your “head on a swivel,” he says, to stay frosty enough to survive, much less thrive.

Although I haven’t performed complete due diligence, Anthony Dilweg seems to be an actual general of the space…someone who is envisioning, positioning and thinking strategically about how to manage through the crisis, while the folks on Wall Street seem to be like Sam above, turning their backs and hoping for the best. I highly recommend this video (linked to the thumbnail). It is the most real talk I’ve heard and it actually made me hopeful. Although I am a very positive person I have been disheartened by the unwillingness of others to pull their head out of the sand and truly confront the issues ahead of us. But, I’m always a little early for better or worse.

Some of the reasons this post is delayed is of course my travel to Denver, Thanksgiving, etc., but part of it is also that I haven’t had enough time to focus on one topic, because as soon as I try, I see another missile hurtling toward me. And focus used to be my thing. Actually, focus used to be our thing, but not so much anymore. I remember when people actually came prepared to meetings for fear of public ridicule, but these days you show up to meetings to go over the information together which is a complete waste of time as people end up processing concepts in real-time without giving matters the deep thought they deserve, often causing strife and unnecessary conflict.

Is this ADD3 by design? It’s a question worthy of pondering. But, for today’s post I’m going to be a little bit all over the place and likely won’t give some topics the attention they deserve, but hope to do so in the coming weeks.

Where to start?

Mr. Cooper/Fidelity Title (FNF)/LoanCare

Although what’s happening at these companies may seem unrelated to the housing market, I believe that this issue could be used as an excuse to halt GSE (Fannie Mae and Freddie Mac) and FHA foreclosures similar to the way “servicer issues” were used to support the recent moratorium for VA loans. Additionally, these events have impacts on the capital markets, so although seemingly a bit off-topic I think these events are important to track for the downstream implications. Inside Mortgage Finance recently reported that the MBA is calling on the Department of Veterans Affairs to provide a plan to the servicers as to how they will be reimbursed for the funds the servicers will have to advance for missed payments while the loans are on hold.

In terms of the cybersecurity incidents, there is still not adequate coverage on this issue. Over six million borrowers are serviced by these companies and no one knows how many closings have been delayed due to the FNF hack. Two more class-action lawsuits have been filed against Mr. Cooper, but we have heard no word on how many customers were impacted or whether they were able to advance enough funds to the GSEs (Fannie Mae and Freddie Mac) to cover payments to the trusts. The GSEs will make sure the trusts are fine, but if Mr. Cooper was short on its remittance, this could have huge implications for them. I have recently talked to a handful of mortgage servicers about this topic. Their response to my questions on the hacks told me everything I need to know - for all the regulation in this space no one is thinking critically. Even though they are required to have business continuity plans, those plans are flat. So, like all tests, they have figured out how to pass with reams of documentation that will be completely meaningless if they get hit.

Bizarrely the most recent news on Mr. Cooper isn’t about the data breach, but right up our alley in that both The Real Deal and The Dallas Morning News are reporting that Mr. Cooper is thinking of giving up 175,000 square feet of office space which, according to both stories, will contribute to Dallas’ growing vacancy problem.

The DFW office market is chilly. Overall vacancy in the office market jumped from 22.8 percent in the third quarter of 2022 to 24.2 percent in the third quarter of 2023..Available sublease space in the market has hovered at 11 million square feet

You may recall that of all cities across the country Dallas, Austin and Houston have a greater percentage of workers who have returned to the office compared to other U.S. markets. Yet, they still have excess office space which supports my theory that this crisis is not just about work-from-home, but also due to our frenzied building spree that started some time ago in the age of cheap debt.

I remember when Mr. Cooper, formerly Nationstar, opened this sparkly building. Quite an improvement from the dingey Class B building they previously inhabited. Its opening heralded Mr. Cooper’s new status as a top dog as the banks effectively exited mortgage.

In other Mr. Cooper news, several AI-generated articles this week seemed to dismiss the breach and the lawsuits, recommending Mr. Cooper’s stock as a top performer in the space. Well, if AI (think robot overlord brains) is bullish on Mr. Cooper then….

Yesterday, we got a sort-of update on Fidelity (top title company) and LoanCare (5th largest servicer) that the hack had been contained. However, the information was limited and many followers told me today they were still unable to make payments:

Shortly after FNF announced the incident, the ransomware group that calls itself ALPHV (also known as BlackCat) listed FNF on its dark web site, effectively claiming responsibility for the cyberattack, and pressuring FNF into paying a ransom to restore operations.

The ransomware gang removed the FNF listing from its leak site on the same day that FNF published its filing, saying it had contained the incident. Sometimes, when listings disappear from a ransomware gang’s websites, it means the victim may have paid the ransom.

Okie dokie. What contained means, or if they paid the ransom, I do not know. I’ve heard from some followers Fidelity was using Gmail to communicate, so that is not a good sign. When the Title industry was hit in 2021 due to a similar breach, I can tell you that it took months for them to truly recover and many did not disclose what had happened. Will we ever know? Likely not, but I do think there will be significant regulatory blowback which could call into question the viability of these companies as a going concern. That, however, will take some time to play out…

Denver

Phew. I just don’t know what to say. Denver seems to be one big new-build site. I’ve heard the knocking of the hammers in my dreams since returning. From multifamily to single-family residential, construction is everywhere….almost as omnipresent as the For Sale and For Lease signs that pepper the once happening Tech Center. When I left Denver in 2019 to move to Pittsburgh, Denver was being touted as the new tech center. It was Austin, before Austin. However, that never fully panned out, and Denver has been in denial ever since.

Below is a horrible video I took of one of the sites. Travis from Real Estate Mindset went out this week and with his drone gathered much better footage (know your strengths), so I hope to share better footage in a deep-dive on Denver next week.

In case you missed it, Travis and I had a great discussion. I highly recommend it as it was an animated deep dive from two industry insiders (despite the goofy thumbnail cover).

More on Denver coming soon.

Home Prices, Inventory and Sundry

FinxTwit is all abuzz with doomy, doomy proclamations from pending sales being the worst since 2001, to existing home sales on track to be the lowest in 30 years, while new home sales and new home prices crater…and then of course this:

H/T - @JuliusMiami

My response? Well, duh. But, based on the recent behavior of the stock market we may find ourselves chopping around for several more months with more ups and downs especially if the downward trend in the 10-year and more long-term rates continues. Depending on how low rates go, the pent-up demand that has been waiting on the sidelines might decide they’ve waited long enough especially as distressed sellers make it worth their while. This could create an interesting dynamic in the spring as both new homes and existing compete for the limited demand.

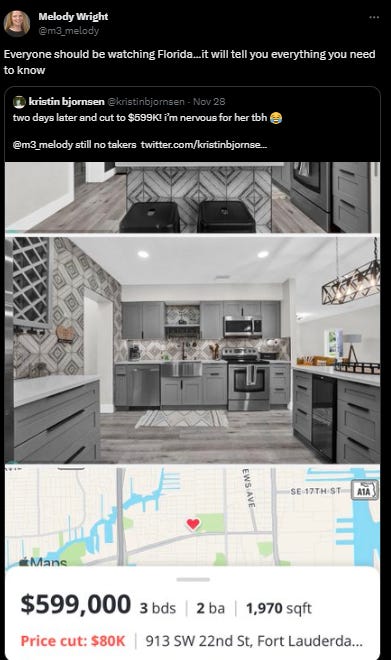

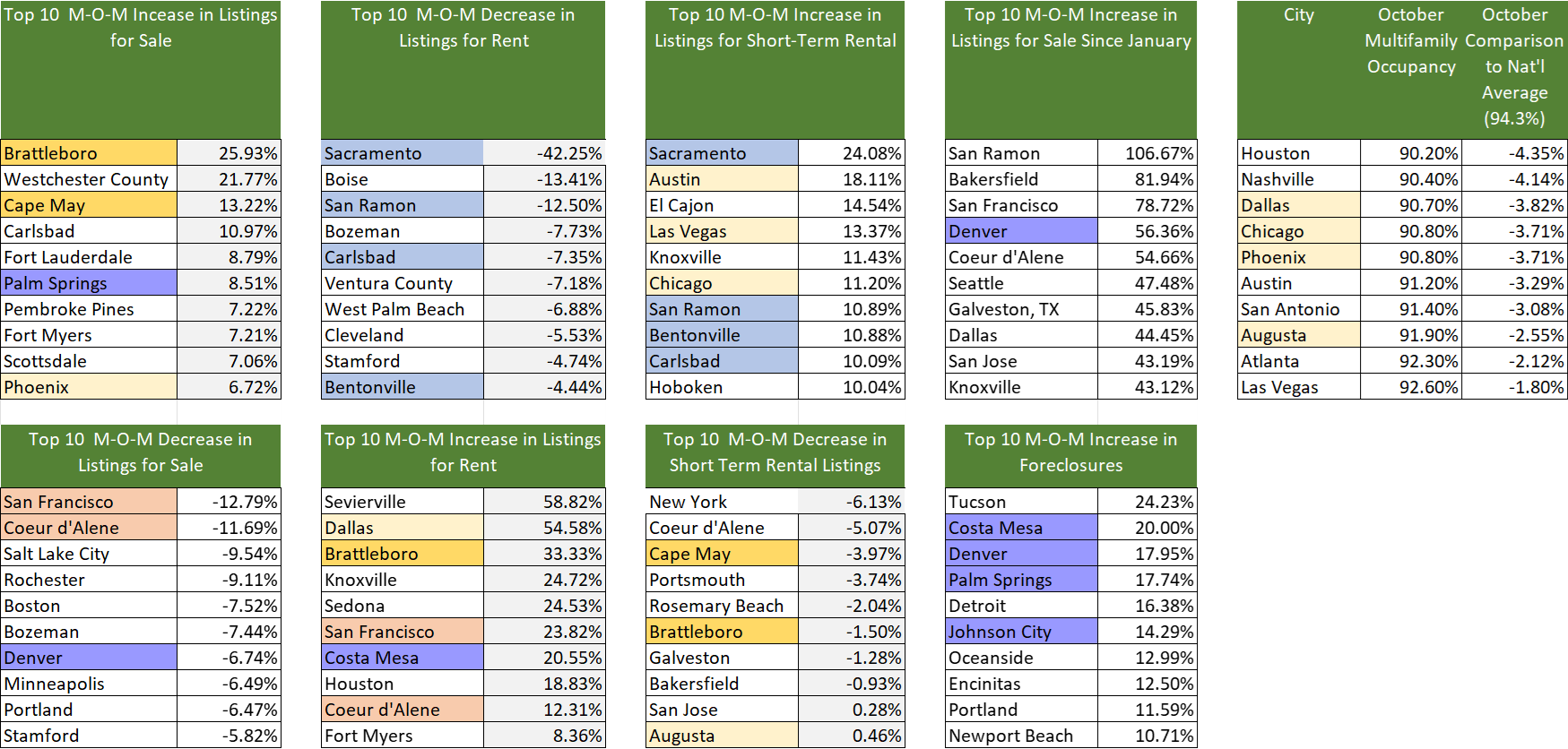

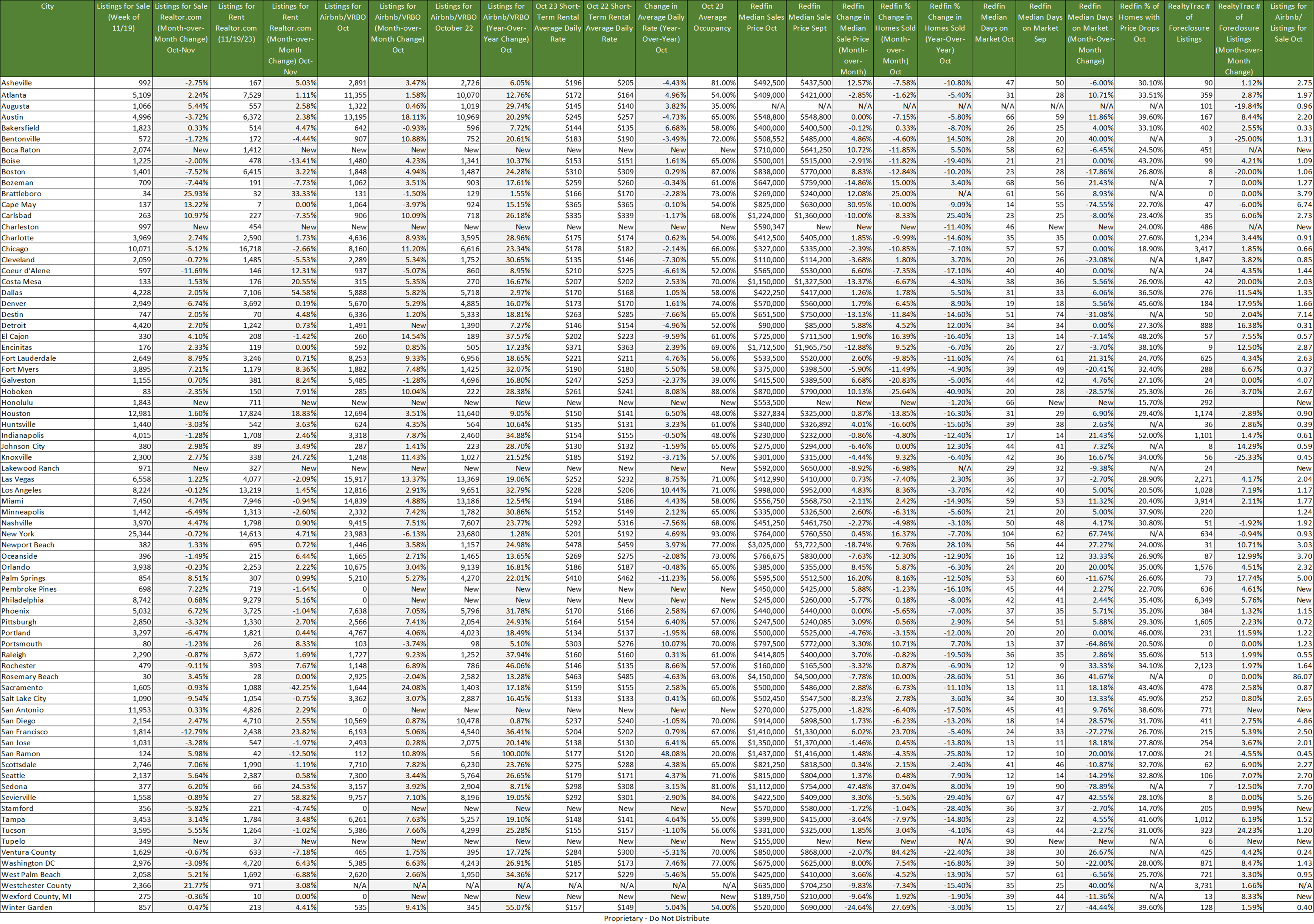

What I’m more focused on right now is watching Florida and the amount of inventory that is scurrying to the listing sites. Inventory has increased on average by 13% since January in the 12 cities I track in Florida, with the biggest, double-digit increases in Rosemary Beach, Ft. Myers, Ft. Lauderdale, Pembroke Pines and Tampa (see monthly summary below for details). Six of those cities reached their highest inventory levels since January last week. Now, in many parts of Florida, according to my realtor friends, this is the buying/selling season for snowbirds. But, what’s interesting is inventory is not decreasing. Additionally, according to Redfin, sales are down on average -11.2% Year-Over-Year and -2% Month-Over-Month while home prices are down on average -2.90%.

More importantly, price cuts are happening as distressed sellers run out of time. I visited the property below with Kristin in August. It was a real lipstick-on-a-pig situation. Located near a substation, five miles from the beach, they enclosed the carport to make an additional bedroom and failed to mention the historic flooding that impacted the area in April. This property was definitely the fever dream of a want-to-be Airbnb jock, but likely low occupancy, property taxes and insurance wiped them out of the game and now they are desperate to offload.

And, for every one home where I see price cuts there are those who are just unwilling to make that first cut as they hold out hope for the Spring season. However, it just takes one seller in a neighborhood to start the journey down the price ladder. If you know your neighbors, it can sometimes be hard to make that first decision. But, when you give up the ghost, you give it up fast. And, what we’ve learned from those existing home sales numbers is that low sales is likely much less to do with inventory and much more to do with affordability and stubbornness (see chart above). People seem to have gotten the memo in a way that they did not in the previous crisis.

Where I am in Johnson City, TN they aren’t as concerned with their neighbors as the story is more about fleeing investors. The listings here are a combination of old apartment buildings, new construction and previous fix-and-flips. New price cuts show up in my inbox each day. Are they enough yet? Not even close. Neighboring Knoxville made it into the top 10 for increases in foreclosure and for increases in inventory since January. Many thought this area would escape unscathed. I think not.

My main message on this topic? Things are indeed turning, but we may find ourselves next year in a continued extend and pretend situation as the powers that be seek to manage the message in the run-up to the election. What do I mean? I believe we will have price drops, but there is a probability they may not be as steep as some expect. Think Florida slowly starting to join its friends in Texas, Arizona and California with the rest of the country still a bit waffly. What could change this? Additional job loss and/or a credit event. I give more probability to the latter scenario, but I think we would be remiss to not consider the other possibility as politicians seek to find flashy ways to mute the crisis. How bad and how quickly things deteriorate in Florida will likely set the pace for the rest of the country. We will also hear about affordable housing ad nauseam next year with few real solutions. Those who are more flexible and forward-looking have already pivoted to that play.

One other phenomenon which may accelerate price drops is the high delinquency I’m hearing about in the private note space (think individuals or small LLCs lending in the shadows) which has escaped the notice of most housing analysts. Another reason I am a bit delayed is that I have been pursuing this story in earnest. More to come soon, but this could be a piece of the puzzle that really changes the game next year. Stay tuned.

Fraud, Lending Standards, The Last Gasp

It is my view we are going to see a lot of perp walks in the near future. Will it be the big actors who escaped justice the last time? Likely not, at least not right away. But, it will be your everyday criminals like this couple in Davie, Florida who took cash from unsuspecting investors for a luxury townhome.

According to the FBI, complaints of mortgage fraud have increased materially:

In 2022, the FBI received 11,727 real estate-related complaints with losses of over $396 million, an 86% increase versus 2020 levels. Earlier this year, the US Secret Service, in conjunction with CertifID Inc., which offers wire fraud protection services, put out an advisory over the “sharp increase in reports of real estate fraud associated with vacant and unencumbered properties.”

Remember that scene in The Big Short when Burry says “and did you know, fraud has been going up.” But, for sure, it’s different this time. In my opinion, the fraud will be worse than anything we’ve seen in our lifetimes. I think most of us still don’t understand the pervasiveness of this mania.

I also have a sneaking suspicion Non-Owner-Occupancy fraud might actually be pursued this cycle. If you are so inclined, this is an excellent blog by the FBI on where you can report fraud.

But, as announced here previously, there are some that keep pushing ahead in these constrained economic conditions on the backs of low-income and vulnerable borrowers, including our government-sponsored enterprises.

Last cycle: They just want a home

This cycle: They just want to increase wealth through investing

Please don’t take the above humor as meaning that homes have become affordable or that everyone who needs a home has a home. We all know that is simply not the case which is what makes the narrative so striking. However you slice it, down payments and loan-limits are there as guardrails to ensure the ability to repay a loan. I have been on the other side of these programs, and the havoc it can wreak on families can be quite detrimental.

And, the GSEs aren’t the only ones piling in to ride the very last pockets of air in the final gasp of this epic COVID boom:

As I say on my YouTube channel each show, there is a lot going on…almost too much to keep track of, making it difficult to know where to focus or spend time. Luckily, I’m not alone and have amazing partners in crime such as dragonslayer, Rudy Havenstein, who puts out great housing content in his posts each week. I encourage you to check out his latest here.

As we round the corner to year-end I think it is important we try and focus on finding joy and fellowship where we can. The holidays are always a mixed bag, and I only know a few who enjoy them completely. One of the things that keeps me from feeling like Sam in the picture above is knowing you all are out there eager for context, alternative perspectives and understanding. I’m extremely grateful for your support.

Until next time….

Monthly & Year-Over-Year Summary Below

The below monthly summary is no-frills (putting it mildly) as the time to compile the data is all the time I have at the moment. I am trying to organize some of the gracious folks who have volunteered to help me flush out all of this data I’ve collected and turn it into pretty charts in a presentation format to facilitate a deeper analysis. Thank you for bearing with me thus far.

For easier viewing of the below images, I would recommend to “Save As” and view with a browser or in a picture viewer.

The color highlights are to help see where cities show up in multiple categories.

Melody, my wife and I were in Georgetown, TX for the holidays. My inlaws bought into Del Webb SunCity. My BIL told me that the price of lots that backed up to a tree line had been reduced from $300k to $100k. I thought that was interesting since they paid $90k for their lot early 2022.

SunCity is a total ripoff.

Dodge ball, and Smear the Queer at recess! Morning In America!